In 2024 the global bond market totaled USD 145.1 trillion. Whereas a decade ago, high-yield bond markets consisted primarily of US issuers, today the market has internationalized with many issuers coming from European and emerging economies. The European high-yield bond market, still less mature than its US counterpart, has more than quadrupled in size since 2008. The emerging economies high-yield corporate segment has experienced tremendous growth and stood at USD 1.46 trillion in Q2/2025, with substantial scope for further growth. Companies in emerging economies primarily use the corporate bond market to refinance existing loans at more favourable terms. Balance sheets of emerging markets corporates frequently show lower leverage than their corporate comparables in development economies, with lower leverage and higher cash-to-debt ratios, while providing more credit spread for equivalent leverage.

The global credit market (bonds and bank loans) in aggregate is about three times the size of the global equity market. This growth has been fuelled by government and corporate debt sales across major developed and emerging economies.

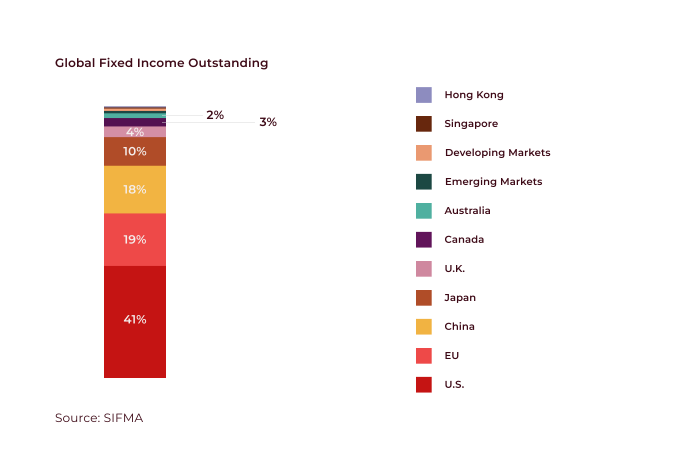

In terms of country of incorporation, global bond markets are dominated by the United States with USD 48.9 trillion in total debt outstanding 2025 of which USD 11.5 trillion in US corporate bonds, and China as the second largest corporate bond market with USD 24.5 trillion, jointly 49 per cent of the total global bond market, of which 53 per cent, is issued by financial institutions. China’s onshore bond market has been estimated at USD 27.5trillion, of which approx. USD 6.95 trillion in onshore corporate bonds. Available data suggest that China holds about 20.5 per cent of its reserves in US Treasury securities.

Challenges persist, and the doors to global capital markets have remained closed for the majority of emerging markets governments and corporates in 2025. Many Sub-Saharan African countries, one of the more volatile markets, have found itself trapped by high interest rates, foreign exchange volatility, and persistent inflation. Market liquidity can be particularly challenging in emerging markets credit markets. Although sovereign Eurobonds offer flexibility compared to traditional conditional loans, they come with higher costs, and shorter maturities. Nigeria expecting to consume nearly 100 per cent of federal revenue for debt repayments in 2026. Ghana’s debt-to-revenue service fell to 25.1 per cent in 2025, from 48 per cent in 2022.

Africa remains an attractive place for investors seeking higher yields compared to other emerging economies. Yields on sovereign bonds in Sub-Saharan Africa are high, with Zambia and Nigeria exhibiting yields of 17.84 and 16.86 per cent for 10Y local currency bonds. Trade is focused on the “spread”, the yield difference between these bonds and US Treasury bonds, with a higher spread indicating higher risks with possible higher returns. Several bonds have been oversubscribed, even in times of default, when a bond is trading higher or lower than anticipated.